Credit Score Explained: What It Is and Why It Matters So Much

What Is a Credit Score?

Feature Video

In today’s financial landscape, few numbers hold as much power over your economic opportunities as your credit score. But what exactly is a credit score? Simply put, it’s a three-digit number ranging from 300 to 850 that represents your creditworthiness. Lenders, banks, and other financial institutions use it to gauge the risk of lending you money. A high score signals reliability, while a low one can signal potential trouble.

The most common models are FICO and VantageScore. FICO, developed by Fair Isaac Corporation, is the gold standard used by 90% of top lenders. VantageScore, created by the three major credit bureaus—Equifax, Experian, and TransUnion—offers an alternative with scores from 300 to 850 as well. Understanding what a credit score is empowers you to take control of your financial future. Keywords like “credit score explained” are searched millions of times monthly because people want clarity on this pivotal metric.

How Credit Scores Are Calculated

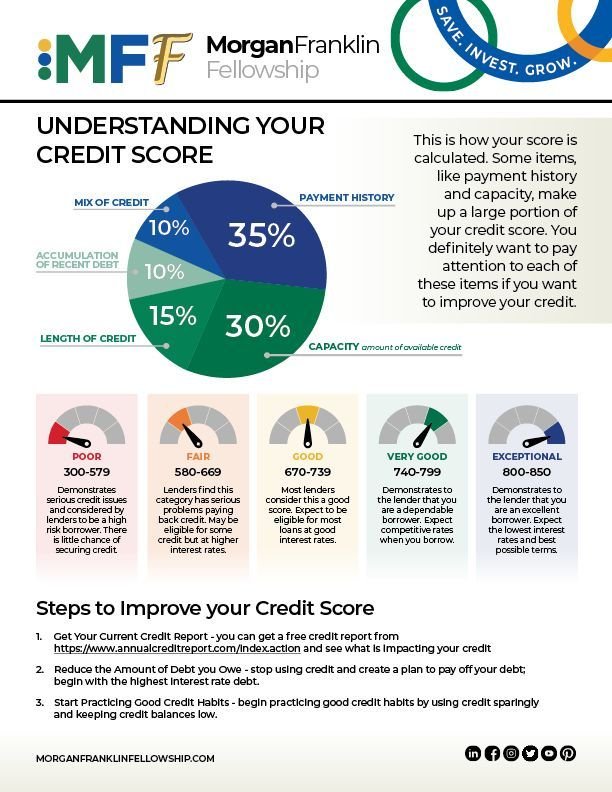

Credit scores aren’t random; they’re calculated using data from your credit reports, which detail your borrowing history. The exact formula is proprietary, but key factors are public knowledge. For FICO, payment history (35%) is king—paying bills on time is crucial. Amounts owed (30%) matter next; high credit utilization (over 30% of available credit) hurts your score.

Length of credit history (15%) rewards long-term borrowers. New credit (10%) penalizes frequent applications, as they suggest risk. Credit mix (10%) favors diversity, like having both revolving (credit cards) and installment (loans) accounts. VantageScore weights are similar but emphasizes payment history even more at 40%.

Your score updates monthly based on bureau reports. Factors like collections, bankruptcies, or late payments can tank it quickly. Regularly monitoring via free annualcreditreport.com or services like Credit Karma helps track changes. Knowing how credit scores are calculated demystifies the process and highlights actionable steps.

Key Factors That Influence Your Credit Score

Diving deeper, payment history is the cornerstone. Even one 30-day late payment can drop your score by 100 points. Aim for autopay to avoid mishaps. Credit utilization ratio is sneaky—pay down balances before statements close to keep it low.

Age of accounts matters; closing old cards shortens history and raises utilization. Hard inquiries from new applications ding scores temporarily (5-10 points), so limit them. Public records like foreclosures linger for seven years but impact fades over time.

Positive actions include becoming an authorized user on a good-standing account or using secured cards if starting fresh. SEO tip: Searches for “factors affecting credit score” spike around tax season, underscoring ongoing interest in optimization.

Why Your Credit Score Matters So Much

Why does a credit score matter so much? It dictates access to life’s big purchases. Mortgages? Excellent scores (740+) snag the best rates, saving thousands over 30 years. For a $300,000 loan, a 760 score might yield 3.5% interest versus 5% for 660—over $100,000 difference in payments.

Auto loans follow suit; poor scores mean higher APRs, inflating costs. Credit cards with rewards? Reserved for high scorers. Even rentals check scores—landlords reject below 650 often. Utilities may demand deposits for low scores.

Employment is impacted too; some employers review credit for finance roles. Insurance premiums rise with low scores, as they’re linked to risk. In short, your credit score is a financial passport—strong ones open doors, weak ones slam them shut.

The Real-World Impact on Loans and Mortgages

Consider loans: Personal loans for debt consolidation or emergencies favor high scores. A 700+ score gets approval fast with low rates; sub-600? Expect denials or payday traps. Mortgages are stricter—FHA allows 580+, but conventional needs 620+. PMI kicks in below 20% down for marginal scores, adding expense.

Refinancing opportunities vanish with poor scores. During economic shifts, like 2023’s rate hikes, pristine scores secured legacy low rates. Why credit score matters for loans: It’s the difference between affordability and financial strain.

Credit Scores and Everyday Life: Rentals, Jobs, and Insurance

Beyond loans, credit scores infiltrate daily life. Apartment hunters face rejections if under 600—some complexes charge higher deposits. Job applicants in banking or government roles disclose scores; red flags raise doubts about fiscal responsibility.

Auto and home insurance? Algorithms factor scores into premiums. Studies show 20-50% hikes for low scores. Cell phone contracts or gym memberships? They check too. A robust score streamlines life; neglect it, and hurdles multiply.

How to Check Your Credit Score for Free

Checking shouldn’t cost. Federal law mandates free weekly reports from AnnualCreditReport.com. Scores? Free via Experian, or apps like Credit Sesame. Banks like Chase or Discover offer complimentary FICO tracking.

VantageScore is free at VantageScore.com. Avoid paid sites unless needed. Discrepancies? Dispute errors online—20% of reports have mistakes fixable in 30 days, boosting scores 20-100 points. Regular checks prevent surprises.

Proven Tips to Improve Your Credit Score

Improving takes time but works. Pay everything on time—set reminders. Reduce utilization below 10% for max boost. Dispute inaccuracies promptly.

Build history with secured cards or credit-builder loans. Avoid new credit during rebuilds. Pay off collections if possible, though “pay for delete” is rare now. Patience pays: Scores rise 100+ points in 6-12 months with discipline.

For rapid gains, bundle payments or use balance transfer cards. Long-term: Diversify credit types responsibly. Tailored advice from NFCC counselors accelerates progress.

Common Credit Score Myths Debunked

Myth 1: Closing cards helps utilization—no, it hurts. Myth 2: Carrying balances builds score—interest accrues without gain. Myth 3: Scores drop yearly checks—soft inquiries don’t count.

Myth 4: Rent/utilities build credit automatically—only if reported. Myth 5: Bankruptcy wipes slate clean—stays 10 years. Busting myths prevents missteps.

Conclusion: Take Control of Your Credit Score Today

Your credit score isn’t just a number—it’s your financial reputation, influencing loans, housing, jobs, and insurance. From understanding what it is to mastering factors and improvement strategies, knowledge is power. Why it matters so much: Opportunities hinge on it.

Start checking reports, pay on time, and lower debt. In 2024’s economy, a stellar score (700+) unlocks best rates amid uncertainty. Empower yourself—your future self will thank you. For more on “credit score explained,” explore resources like CFPB.gov.

(Word count: 1217)