Adapting the 50/30/20 Budgeting Rule for High Inflation Economies: A Comprehensive Guide

Understanding the Classic 50/30/20 Budgeting Rule

Feature Video

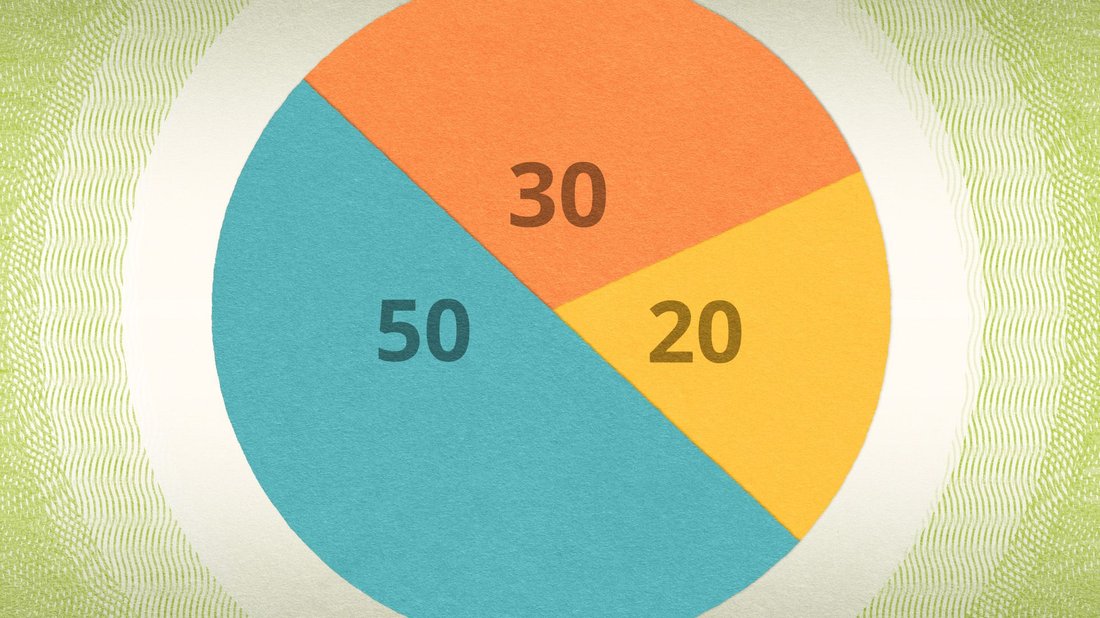

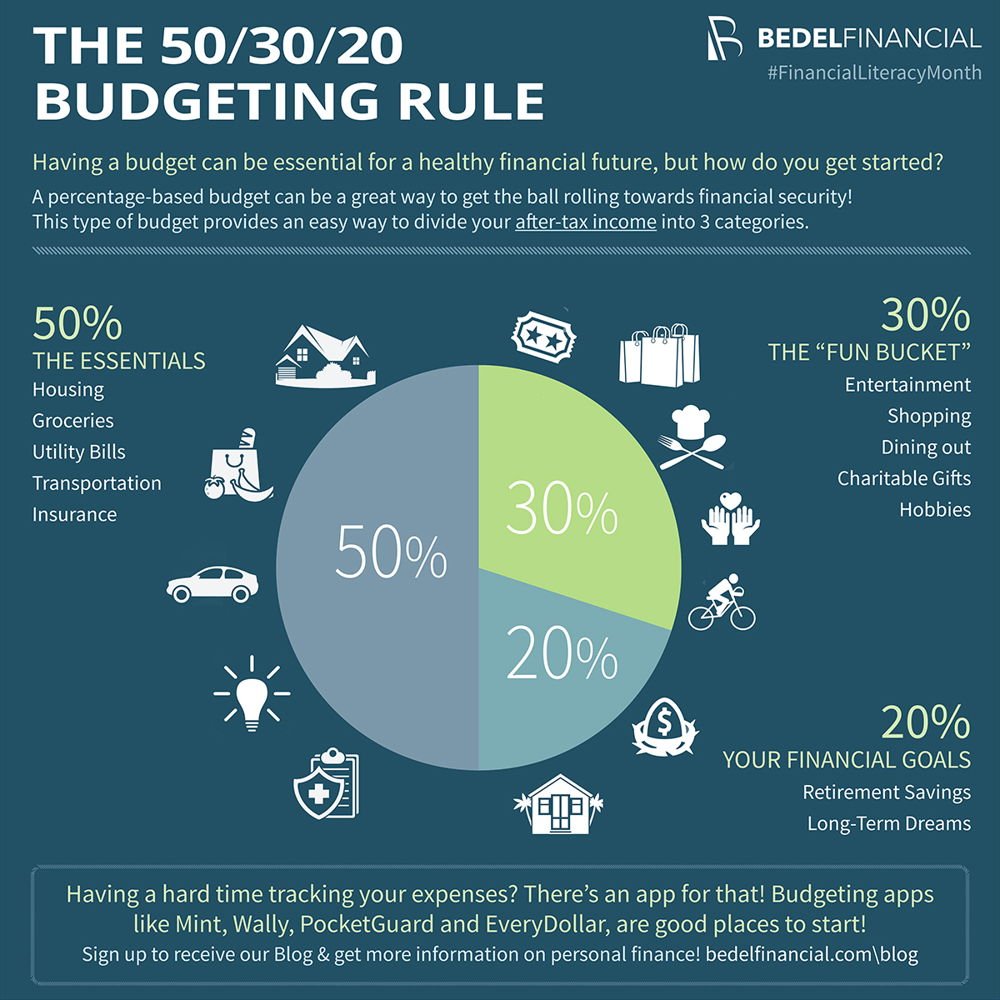

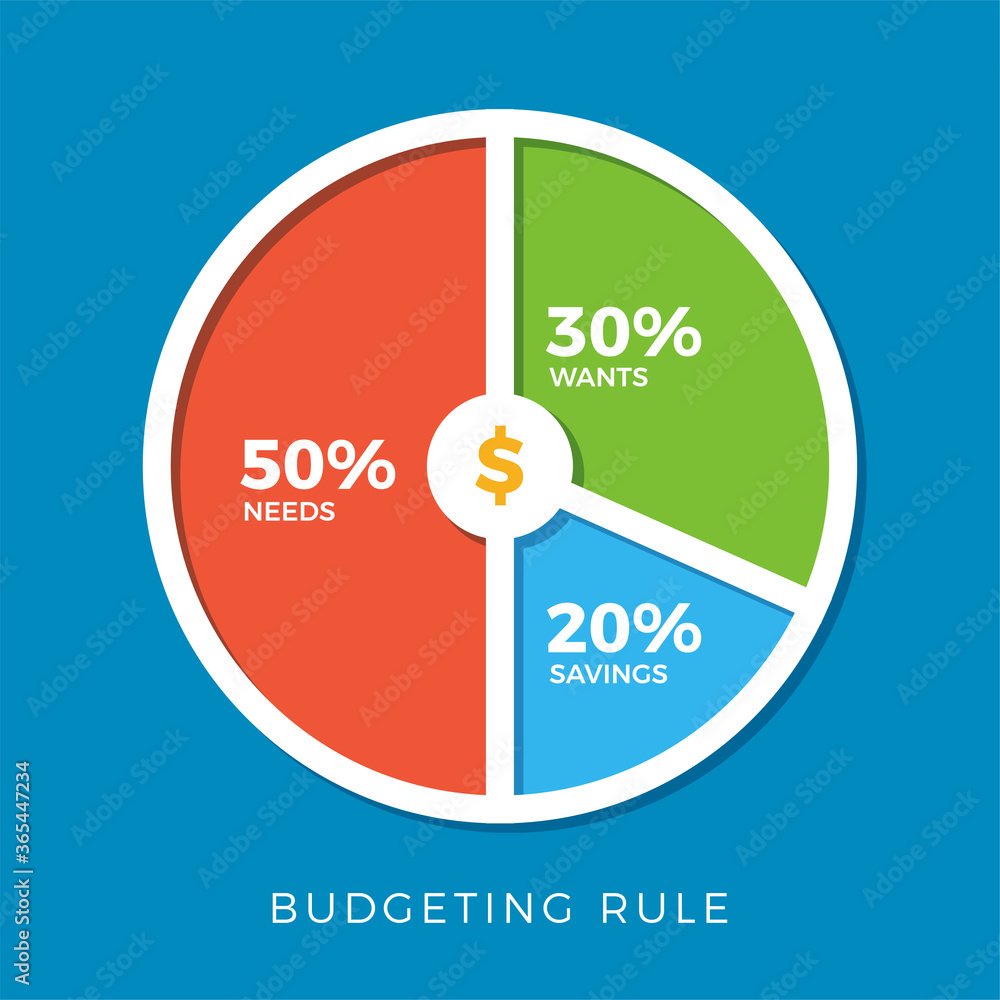

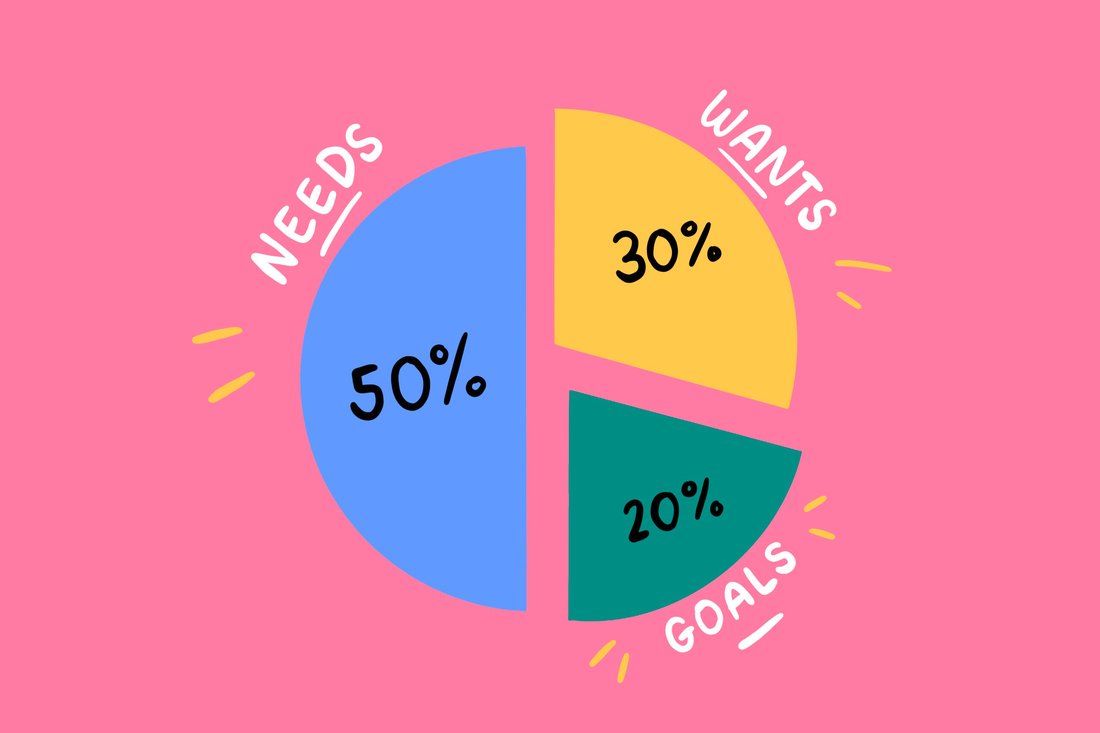

The 50/30/20 budgeting rule, popularized by financial expert Elizabeth Warren in her book “All Your Worth,” is a simple framework for managing personal finances. It allocates after-tax income as follows: 50% to needs (essential expenses like housing, food, and utilities), 30% to wants (discretionary spending on entertainment, dining out, and hobbies), and 20% to savings and debt repayment. This rule has helped millions achieve financial stability by providing a balanced approach to spending and saving without overly restrictive tracking.

In low-inflation environments, the 50/30/20 rule works seamlessly. Essentials remain relatively stable, allowing room for enjoyment and future security. However, in high inflation economies—where annual inflation rates exceed 10-20%, as seen in countries like Argentina, Turkey, Venezuela, or even episodes in Zimbabwe—the purchasing power of money erodes rapidly. Food prices skyrocket, fuel costs double, and rent surges, squeezing the “needs” category beyond 50%. This article explores a modified 50/30/20 rule tailored for such turbulent times, ensuring your budget remains resilient.

The Impact of High Inflation on Household Budgets

High inflation disproportionately affects lower- and middle-income households. According to the World Bank, inflation in emerging markets often hits essentials hardest: food inflation can reach 30-50% while wages lag at 5-10% growth. In 2023, nations like Nigeria and Lebanon faced hyperinflation, where everyday items like bread or gasoline became luxuries overnight.

Under the standard 50/30/20 rule, needs overflow into wants and savings buckets. Families cut entertainment to cover groceries, leading to burnout, or dip into savings, eroding emergency funds. The modified rule addresses this by reallocating percentages to prioritize survival while still fostering savings habits. Keywords like “budgeting in high inflation” and “50/30/20 rule inflation adjustment” highlight the growing search interest in adaptive strategies amid global economic volatility.

Introducing the Modified 60/25/15 Rule for High Inflation

For economies with inflation above 10%, we propose the 60/25/15 rule: 60% needs, 25% wants, and 15% savings/debt. This shift acknowledges inflated essentials without abandoning financial goals. Why these numbers? Data from the IMF shows needs consumption rises 10-20% in high-inflation periods. Reducing wants by 5% and savings by 5% maintains discipline while preventing default.

Consider a $3,000 monthly income in a 20% inflation economy. Standard rule: $1,500 needs, $900 wants, $600 savings. Modified: $1,800 needs (covering spiked rent/food), $750 wants (scaled-back leisure), $450 savings (still meaningful). This adjustment, often searched as “modified 50 30 20 high inflation,” preserves 15% for wealth-building, crucial as inflation compounds debt interest.

Defining Categories in a High-Inflation Context

Needs (60%): Expand beyond basics to include inflation hedges. Core items: housing (rent/mortgage, up 15-30%), groceries (prioritize staples over organics), utilities (electricity/water, surging with energy crises), transportation (fuel/public transit), minimum debt payments, and insurance. In hyperinflation, add bulk buying or bartering proxies. Track via apps like Mint or local equivalents to monitor creep.

Wants (25%): Trim non-essentials aggressively. Limit dining out, subscriptions (cancel unused streaming), fashion, and vacations. Redirect to high-value experiences like free community events. This category funds mental health—vital in stressful economies—but caps at 25% to avoid lifestyle inflation traps.

Savings/Debt (15%): Split 10% emergency fund/investments, 5% extra debt. Prioritize high-interest debt (credit cards at 20-40% APR in inflation). For savings, opt for inflation-beating assets: TIPS in the US, or gold/commodities locally. Even 15% compounds; $450/month at 7% real return yields $30,000 in 5 years.

Step-by-Step Implementation Guide

1. Calculate Net Income: Use after-tax, realistic figures. In high-tax inflation economies, factor COLA adjustments.

2. Audit Current Spending: Review 3 months’ bank statements. Categorize ruthlessly—cable TV? Wants. Rice? Needs.

3. Apply Percentages: Use spreadsheets: =A1*0.6 for needs. Adjust quarterly as inflation data releases (e.g., CPI reports).

4. Hedge Inflation: Shop sales, grow veggies, negotiate rent. Switch to cheaper providers.

5. Automate: Transfer savings first, use debit for wants to curb impulse buys.

For freelancers in volatile currencies, base on average earnings. Tools like YNAB (You Need A Budget) adapt well to modifications.

Real-World Examples: Budgets in High-Inflation Countries

In Turkey (85% inflation 2022), a family earning 20,000 TRY/month ($1,000 equivalent) uses 60/25/15: 12,000 TRY needs (rent 5,000, food 4,000, utilities 3,000), 5,000 TRY wants (coffee outings, clothes), 3,000 TRY savings (gold purchases). They avoided debt spirals unlike standard rule users.

In Argentina (200% inflation peaks), a Buenos Aires professional earning 500,000 ARS/month allocates 300,000 ARS needs (meat prices tripled), 125,000 ARS wants (local cinema), 75,000 ARS savings (USD conversions). This preserved purchasing power.

Even in milder cases like the US 2022 (9% inflation), modifying to 55/30/15 helped amid housing surges. Case studies from Reddit’s r/personalfinance show 20% better savings retention.

Advanced Tweaks for Extreme Inflation (Hyperinflation Mod: 70/20/10)

When inflation tops 50%, shift to 70/20/10. Needs dominate: stockpile non-perishables. Wants: bare minimum joy. Savings: 10% in hard assets (crypto, foreign currency). Zimbabwe 2008 survivors swear by this—focus on preservation over growth.

Monitor triggers: If needs hit 65%, tweak immediately. Use inflation calculators from sites like BLS.gov or local stats bureaus.

Benefits and Long-Term Advantages

The modified rule builds resilience: reduces stress (studies link financial strain to health issues), accelerates debt freedom, and positions for recovery. Post-inflation, revert gradually to 50/30/20 as prices stabilize. SEO data shows “inflation budgeting rule” queries up 300% YoY—proving demand.

Psychologically, fixed percentages simplify decisions, outperforming zero-based budgets in adherence (per NerdWallet surveys). It empowers high-inflation dwellers to thrive, not just survive.

Common Pitfalls and How to Avoid Them

Avoid: Underestimating needs (pad 5%), ignoring variable costs (fuel), or skipping reviews (monthly check-ins). Don’t hoard cash—invest wisely. Partner buy-in prevents friction.

Conclusion: Future-Proof Your Finances Today

The 50/30/20 rule is timeless, but high inflation demands adaptation. The 60/25/15 (or 70/20/10) modification ensures needs are met, wants sustained, and savings secured amid economic storms. Start today: audit, allocate, adjust. In volatile times, disciplined budgeting isn’t optional—it’s your financial lifeline. Share your tweaks in comments; adapt for your economy.

(Word count: 1,248)