How to Boost Your Credit Score by 100 Points in Six Months

Understanding Your Credit Score and Why It Matters

Feature Video

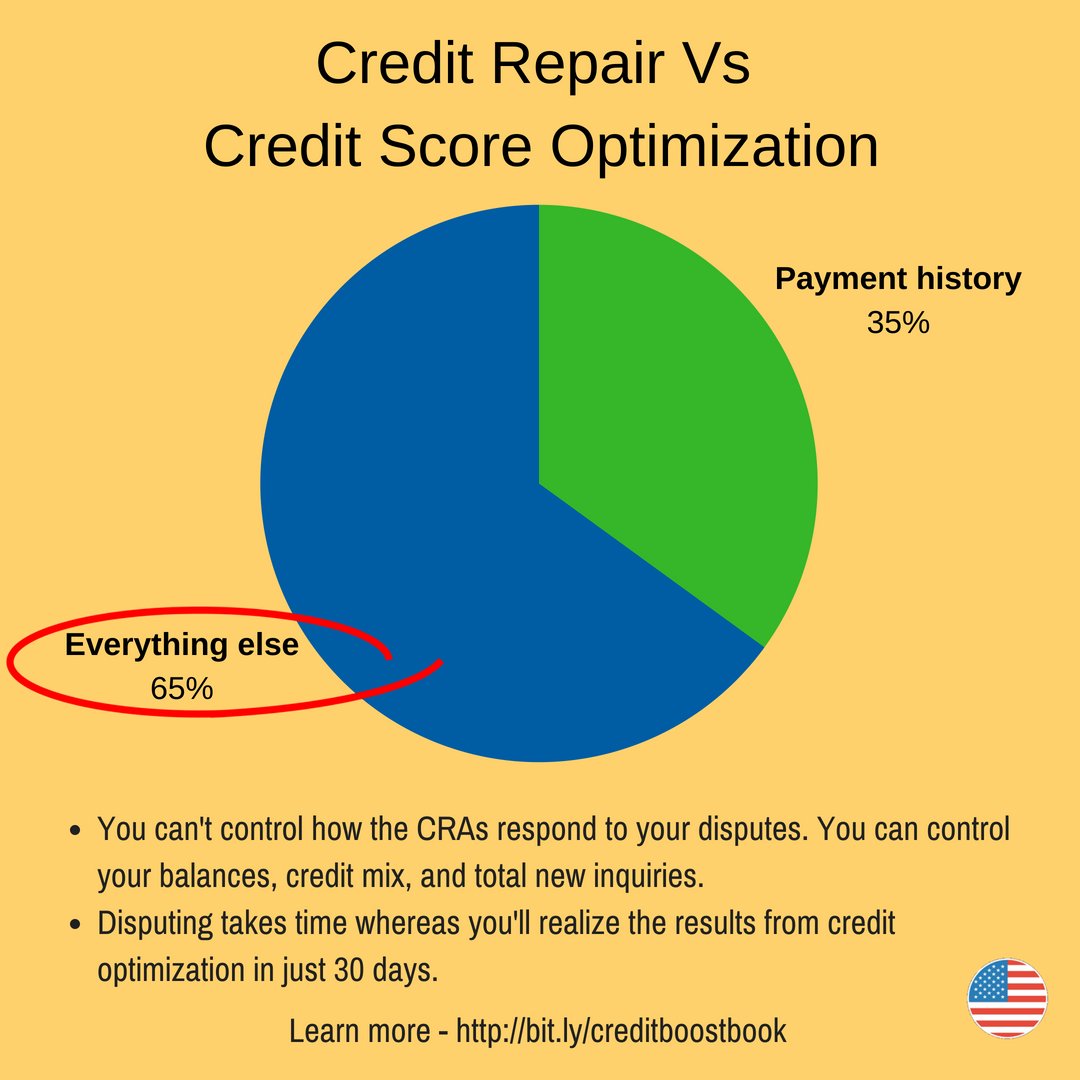

Your credit score is a three-digit number that lenders use to assess your creditworthiness. Ranging from 300 to 850, a higher score means better loan terms, lower interest rates, and more financial opportunities. Boosting your score by 100 points in six months is ambitious but achievable, especially if you start from a fair range (around 600-669). Factors like payment history (35%), credit utilization (30%), length of credit history (15%), new credit (10%), and credit mix (10%) influence it. This guide outlines proven strategies to make significant improvements quickly. By following these steps diligently, you can see results within weeks, with compounding effects over six months.

Step 1: Pull Your Free Credit Reports and Scores

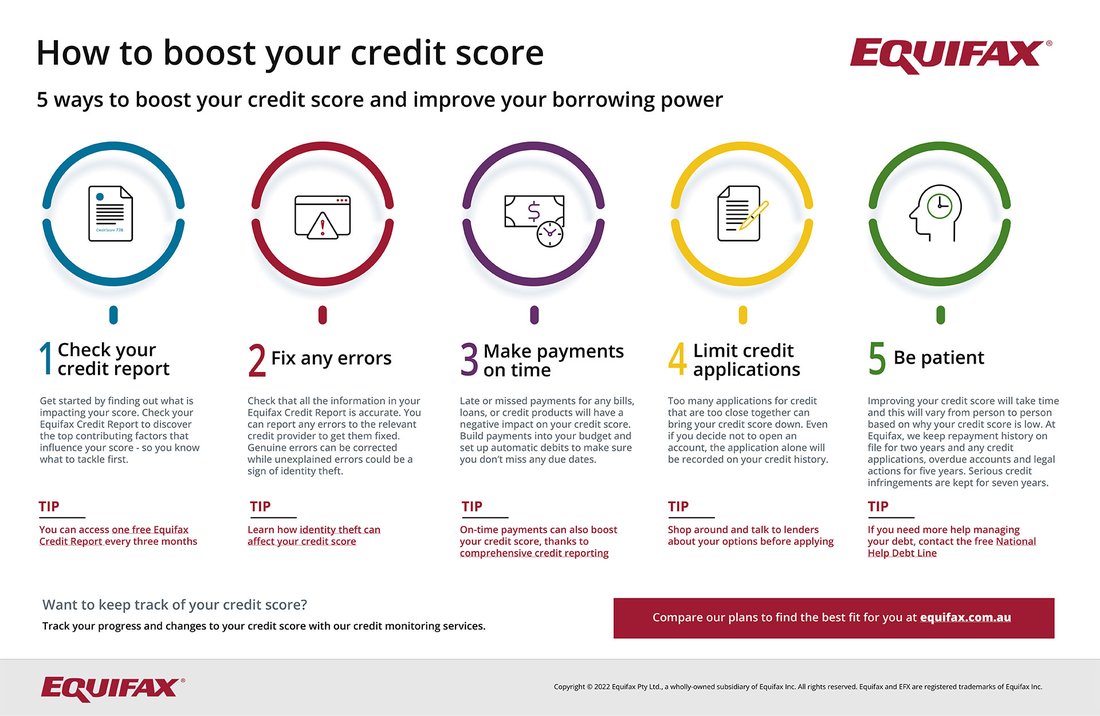

The first step to boosting your credit score is knowing where you stand. Obtain free weekly credit reports from AnnualCreditReport.com, authorized by federal law. Check reports from Equifax, Experian, and TransUnion for discrepancies. Use free tools like Credit Karma or Credit Sesame for ongoing score monitoring. Identify errors such as incorrect late payments, fraudulent accounts, or outdated information. A single error correction can boost your score by 20-100 points instantly. Spend a day reviewing each report meticulously—accuracy here sets the foundation for your six-month plan.

Understanding your current score helps set realistic goals. If you’re below 600, focus on basics; above 650, target utilization and inquiries. Track your progress monthly to stay motivated. This initial audit alone can reveal quick wins, potentially adding 50 points before you implement other changes.

Step 2: Dispute Inaccurate Information Aggressively

Errors on credit reports are common—up to 25% have mistakes per FTC studies. Dispute inaccuracies online via each bureau’s portal or by mail with supporting documents. Common issues include wrong personal info, duplicate accounts, or collections past the seven-year mark. Be detailed in your disputes; vague claims get ignored. Bureaus must investigate within 30 days, often removing invalid items.

For example, if a paid collection lingers, provide proof of payment. Successful disputes average 20-60 point gains. Repeat every 30 days if needed. Tools like DisputeBee or Lexington Law can automate this for complex cases, but start DIY to save money. This step is low-effort, high-reward, often yielding the fastest 100-point jumps.

Step 3: Establish Perfect Payment Habits

Payment history is the biggest factor. Late payments drop scores by 100+ points and linger seven years. Set up autopay for all bills—credit cards, loans, utilities. Pay at least the minimum on time, every time. Use calendar reminders or apps like Mint for due dates. If behind, negotiate with creditors for “pay-for-delete” on recent lates or goodwill adjustments.

Aim for zero lates in six months. Positive history builds rapidly; three months of on-time payments can recover from a single late. Prioritize revolving debt. This habit alone can net 50-100 points as bureaus update monthly.

Step 4: Slash Your Credit Utilization Ratio

Utilization—credit used vs. available—impacts 30% of your score. Keep it under 30%, ideally 10%. If you have $10,000 limits and $4,000 balances, utilization is 40%—too high. Pay down balances aggressively. Request credit limit increases after six on-time payments (without hard inquiries if possible). Avoid closing old accounts, as it raises utilization.

Strategy: Pay cards twice monthly. For a $5,000 balance on $10,000 limit, dropping to $1,000 (10%) could add 50-80 points. FICO simulates: from 80% to 10% utilization boosts fair scores dramatically. In six months, consistent low utilization compounds gains.

Step 5: Avoid New Credit Applications and Hard Inquiries

New inquiries ding scores 5-10 points each, lasting 12 months. Limit to essentials. Rate-shop mortgages/auto loans within 14-45 days (counts as one inquiry). Pre-qualify softly first. Don’t open store cards or unnecessary lines—tempting but counterproductive.

Build score organically. If thin credit, consider secured cards like Discover it Secured (no annual fee, potential upgrade). Six months without inquiries preserves gains from other steps.

Step 6: Tackle Collections and Charged-Off Accounts

Collections crush scores. Pay or settle them, negotiating pay-for-delete (PFD) letters. Not all honor PFD, but try. Recent collections hurt more; older ones less. Use debt validation letters if questionable.

For charged-offs, same approach. Clearing three collections could add 50-100 points. Prioritize newest/highest-balance. Track via reports; updates take 30-60 days.

Step 7: Leverage Credit-Building Tools and Strategies

Boost with authorized user status on a family member’s excellent card (notify issuer for reporting). Use Experian Boost for utility/phone payments. Credit builder loans from Self or Credit Strong report positive history.

Mix accounts: Keep installment (loans) and revolving open. Piggybacking or seasoning new accounts helps. These add diversity, lifting scores 20-50 points.

Step 8: Monitor, Maintain, and Stay Consistent

Track weekly via apps. Scores update variably—TransUnion fastest. Six-month timeline: Months 1-2 for disputes/payments (50 points), 3-4 utilization (30 more), 5-6 habits solidify (20+). Avoid lifestyle inflation; budget via YNAB.

Realistic? Yes, from 620 to 720 possible per myFICO forums. Patience key—FICO VantageScore slower.

Common Pitfalls to Avoid

Don’t close paid cards (shortens history). Ignore debt settlement scams. Bankruptcy last resort. Bankruptcy hurts long-term but can help if overwhelmed.

Long-Term Maintenance After Six Months

Once at goal, sustain: 1% utilization, annual checks, emergency fund. Good score saves thousands in interest.

Conclusion: Your Path to a 100-Point Boost

Boosting 100 points demands discipline but transforms finances. Start today: reports, disputes, payments. In six months, reap rewards—better rates, approvals. Consult NFCC counselors if needed. Your future self thanks you.

(Word count: 1215)