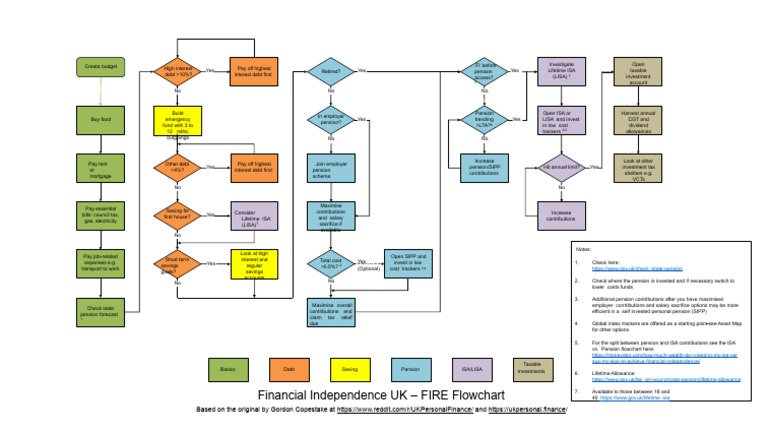

The Financial Independence (FIRE) Movement: A Beginner’s Guide

What is the FIRE Movement?

Feature Video

The Financial Independence, Retire Early (FIRE) movement has taken the personal finance world by storm, captivating millennials, Gen Z, and even some boomers who dream of escaping the traditional 9-to-5 grind. At its core, FIRE is a lifestyle strategy aimed at achieving financial independence—where your investments generate enough passive income to cover living expenses—allowing you to retire decades earlier than the conventional age of 65. This beginner’s guide to the FIRE movement will break down its principles, strategies, and real-world applications to help you decide if it’s right for you.

Financial independence means your savings and investments work for you, not the other way around. The “retire early” part is flexible; for some, it means quitting work entirely at 40, while for others, it involves pursuing passion projects or part-time gigs. Popularized online through blogs like Mr. Money Mustache and forums such as Reddit’s r/financialindependence, FIRE emphasizes frugality, aggressive saving, and smart investing. Keywords like “FIRE calculator,” “retire early strategies,” and “passive income streams” dominate searches as more people seek ways to build wealth quickly in an era of stagnant wages and rising costs.

The Origins and Rise of FIRE

The FIRE movement traces its roots to the 1990s with authors like Vicki Robin and Joe Dominguez in “Your Money or Your Life,” which introduced the idea of calculating your “real hourly wage” and prioritizing time over money. It exploded in the 2010s amid economic uncertainty post-2008 recession. Influential bloggers like Pete Adeney (Mr. Money Mustache) shared how he and his wife retired in their 30s after saving 50-70% of their income.

Social media amplified FIRE’s reach. Podcasts like “ChooseFI” and books such as “The Simple Path to Wealth” by JL Collins made complex concepts accessible. Today, with inflation and housing crises, searches for “FIRE movement explained” have surged, reflecting a generational shift toward financial sovereignty. The movement’s appeal lies in its data-driven approach: using tools like the 4% safe withdrawal rule from the Trinity Study, adherents aim to save 25 times their annual expenses.

Types of FIRE: Finding Your Flavor

Not one-size-fits-all, FIRE has variants tailored to different risk tolerances and lifestyles. Lean FIRE involves extreme frugality, targeting $40,000 or less in yearly expenses for minimalists. For example, living on $1,000/month in a low-cost area requires saving $1 million at a 4% withdrawal rate.

Fat FIRE suits those wanting luxury post-retirement, saving for $100,000+ annual spending—often 30-50 times expenses. Barista FIRE blends part-time work (like coffee shop gigs) with investments to bridge gaps, ideal for healthcare coverage. Coast FIRE means front-loading savings early, then coasting on career growth while investments compound. Finally, Dream FIRE focuses on dream lifestyles, like world travel, without rigid numbers.

Choosing a type starts with tracking expenses via apps like Mint or YNAB. SEO tip: Searches for “Lean FIRE vs Fat FIRE” highlight the need for personalized paths in your FIRE journey.

Step-by-Step Guide to Achieving FIRE

Ready to ignite your FIRE? Follow these proven steps. First, calculate your FIRE number: annual expenses x 25. If you spend $40,000/year, aim for $1 million. Use online FIRE calculators for projections based on savings rate and returns.

Step 1: Boost income. Side hustles, career advancement, or entrepreneurship can double earnings. High earners accelerate FIRE fastest.

Step 2: Slash expenses ruthlessly. The 50/30/20 rule evolves to 50/10/40 (needs/wants/savings). Cut housing (under 25% income), transportation, and dining out. Mr. Money Mustache advocates biking and DIY everything.

Step 3: Invest aggressively. Max tax-advantaged accounts: 401(k)s, IRAs, HSAs. Index funds like VTSAX offer low-fee, broad-market exposure. Historical 7% real returns (after inflation) power compounding. Dividend stocks or real estate provide passive income.

Step 4: Track progress quarterly. Adjust for life changes like kids or health issues. Build a 3-6 month emergency fund first.

A 50% savings rate could achieve FIRE in 17 years; 70% in 10. Tools like Personal Capital visualize net worth growth, optimizing your path to financial freedom.

Key Strategies and Tools in the FIRE Arsenal

Central to FIRE is the 4% rule: withdraw 4% of your portfolio annually, adjusted for inflation, with 95% historical success over 30 years. Critics note sequence-of-returns risk in early retirement, suggesting 3-3.5% for safety.

Real estate investing via rentals or REITs diversifies beyond stocks. Geo-arbitrage—moving to low-cost countries like Thailand—stretches dollars. Side incomes like blogging or Uber persist into semi-retirement.

Tech aids abound: Empower for fee analysis, Vanguard for funds, and FIRE-specific apps like “FI Dashboard.” Behavioral finance matters too—avoid lifestyle inflation via “no buy” challenges.

Pros and Cons of Pursuing FIRE

Pros: Time freedom, stress reduction, pursuit of purpose. Early retirees report higher life satisfaction, traveling or volunteering unbound by jobs.

Cons: Sacrifices social life (frugality isolates), market risks (downturns delay retirement), healthcare hurdles pre-Medicare. Critics call it privileged—requiring education and stable jobs. Burnout from grinding savings is real; many “retire” then return to work.

Balanced view: FIRE builds discipline applicable sans full retirement, like debt freedom or dream funding.

Real-Life FIRE Success Stories

Meet the Pfau family, Fat FIRE achievers in their 30s via tech salaries and index investing. Or Sam Dogen of Financial Samurai, retired at 34 after $3M net worth. Women like Mad Fientist’s partner prove it’s unisex. Diverse stories on BiggerPockets forums show rentals accelerating timelines.

These tales inspire, but remember: average timelines are 10-20 years with discipline.

Common Myths Debunked

Myth 1: FIRE is only for six-figure earners. No—low earners succeed via frugality and time.

Myth 2: You’ll be miserable skimping. Many thrive on less, valuing experiences.

Myth 3: Markets always rise. Diversify and plan conservatively.

Is FIRE Right for You? Next Steps

Assess your risk tolerance, values, and patience. Start small: save 20%, read “The Psychology of Money,” join communities. FIRE isn’t a race—it’s reclaiming life control.

In conclusion, the FIRE movement democratizes wealth-building, proving early retirement possible with math, not magic. Whether Lean or Fat, it empowers beginners to dream big. Track “financial independence retire early” progress today—your future self thanks you. (Word count: 1,248)