The 50/30/20 Budgeting Rule: A Simple Plan for Financial Control

What is the 50/30/20 Budgeting Rule?

Feature Video

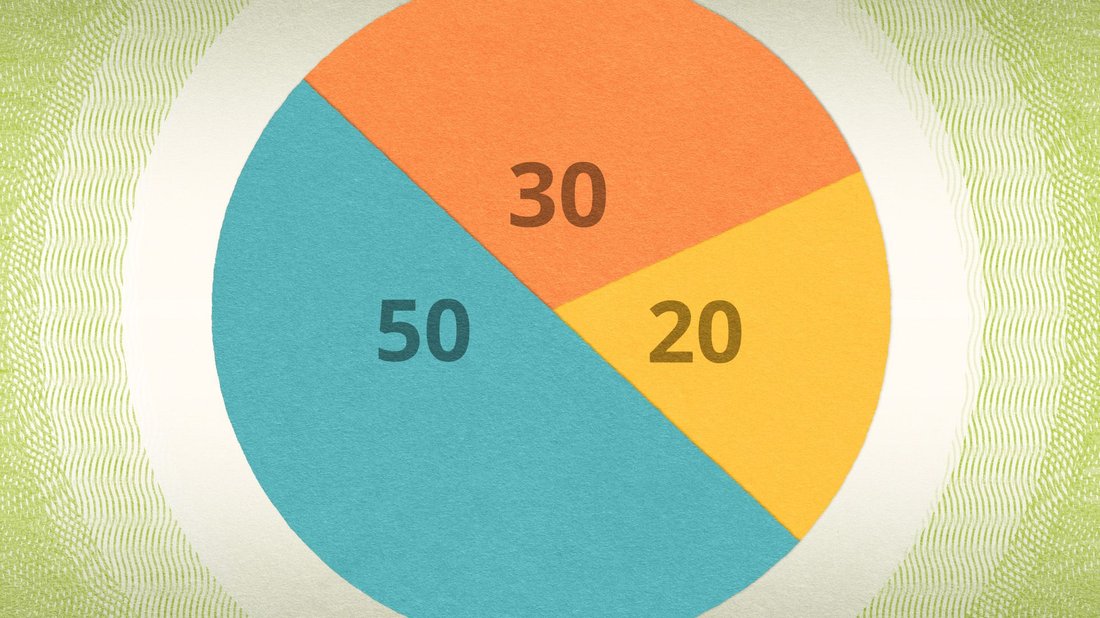

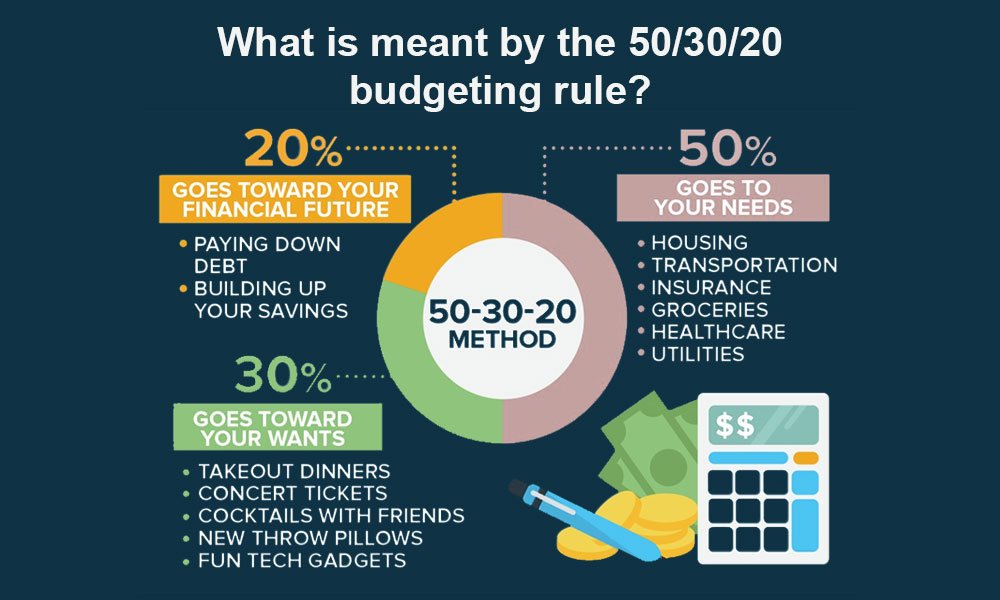

The 50/30/20 budgeting rule is a straightforward and effective framework for managing personal finances, popularized by financial expert Elizabeth Warren in her book “All Your Worth: The Simple and Radical Way to Develop a Fly-Budget—and Spend Like a Boss.” This rule divides your after-tax income into three simple categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It’s designed for anyone seeking financial control without complex spreadsheets or restrictive diets.

In today’s economy, where inflation and rising costs challenge household budgets, the 50/30/20 rule offers a balanced approach. Unlike rigid zero-based budgeting, it allows flexibility while promoting discipline. By allocating percentages rather than fixed dollars, it adapts to income fluctuations, making it ideal for freelancers, salaried workers, or families. Search trends show millions querying “50/30/20 rule” monthly, proving its popularity as a go-to strategy for financial stability.

At its core, this rule ensures essentials are covered, lifestyle enjoyed, and future secured. Whether you’re drowning in debt or building wealth, implementing the 50/30/20 budgeting rule can transform your money mindset.

Breaking Down the 50/30/20 Categories

The beauty of the 50/30/20 budgeting rule lies in its clear categorization. Let’s dissect each segment for better understanding.

50% Needs: This chunk covers non-negotiable expenses required for survival and basic functionality. Think housing (rent or mortgage under 30% of income ideally), utilities, groceries, transportation (car payments, gas, public transit), minimum debt payments, insurance, and healthcare. The goal is to keep these under half your take-home pay. If needs exceed 50%, it’s a red flag—time to downsize housing or refinance debts.

For a household earning $5,000 monthly after taxes, needs cap at $2,500. This prevents lifestyle inflation, where spending rises with income, trapping many in the paycheck-to-paycheck cycle. Track via apps like Mint or YNAB to identify leaks.

30% Wants: Here’s where fun enters. Wants include dining out, entertainment, hobbies, subscriptions (Netflix, gym), vacations, and non-essential shopping. This 30% fuels joy without guilt, preventing burnout from frugality. However, it’s not a blank check—prioritize high-value experiences over impulse buys.

In the $5,000 example, allocate $1,500. If you’re a coffee enthusiast, brew at home and splurge occasionally. This category teaches discernment, aligning spending with values.

20% Savings and Debt: The powerhouse for wealth-building. Direct this to emergency funds (3-6 months’ expenses), retirement (401(k), IRA), investments (stocks, index funds), or extra debt payments beyond minimums. High-interest debt first (credit cards over 15%), then low-interest like student loans.

For $5,000 income, that’s $1,000 monthly—compounding to $150,000+ in a decade at 7% returns. Automate transfers on payday for effortless progress.

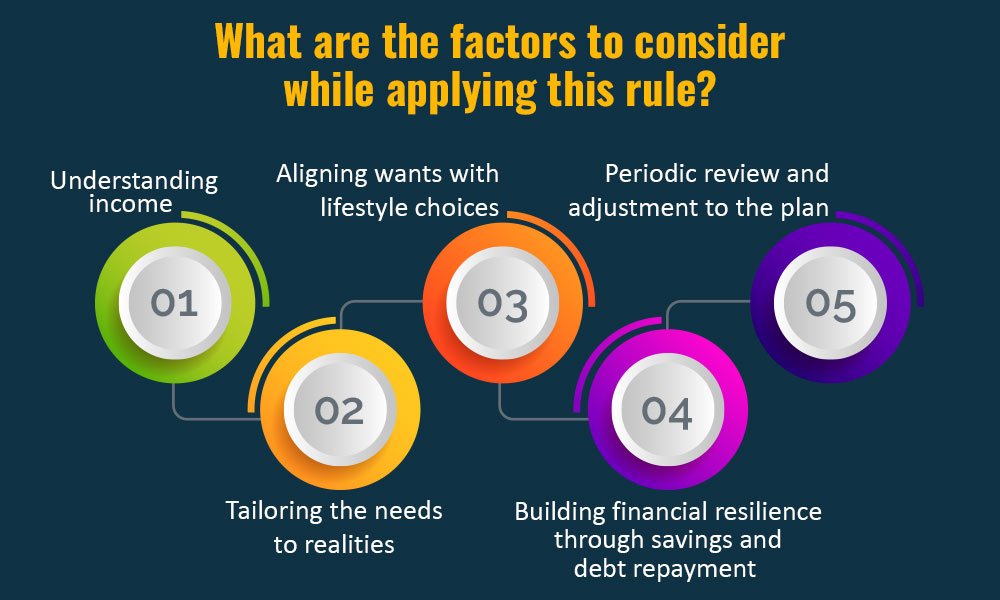

How to Implement the 50/30/20 Budgeting Rule Step-by-Step

Starting the 50/30/20 rule is simple. Follow these steps for seamless adoption.

Step 1: Calculate Take-Home Pay. Use net income (after taxes, deductions). Tools like paycheck calculators help. Annualize if irregular.

Step 2: List Expenses. Review 3 months’ bank statements. Categorize into needs, wants, savings/debt. Be honest—gym membership a need or want?

Step 3: Set Limits. Multiply net pay by 0.50, 0.30, 0.20. Adjust categories if over/under. Example: If needs hit 60%, cut housing or utilities.

Step 4: Track and Adjust. Use apps (PocketGuard, Goodbudget) or spreadsheets. Review weekly. Life changes? Recalibrate monthly.

Step 5: Automate Everything. Bill pay for needs, transfers to savings. Prepaid cards for wants limit overspending.

Real-world tip: Start small. If 50/30/20 feels tight, try 60/25/15 initially, scaling up. Consistency beats perfection.

Benefits of the 50/30/20 Budgeting Rule

Why choose 50/30/20 over other methods? Its benefits are profound and research-backed.

First, simplicity. No daily logging needed. Harvard studies show simple rules outperform complex plans for adherence.

Second, balance. Unlike Dave Ramsey’s debt snowball (extreme cuts), it sustains motivation. A 2023 NerdWallet survey found 70% of users happier post-adoption.

Third, financial security. Prioritizing 20% savings builds buffers against recessions. During COVID, those with emergency funds fared better.

Fourth, scalability. Works for $30K earners (needs $1,250) or $100K+ households. Adjusts for high-cost areas (e.g., 40/40/20 in NYC).

Fifth, mindset shift. Encourages intentionality, reducing buyer’s remorse. Long-term, it accelerates goals like homeownership or retirement.

Real-Life Examples of the 50/30/20 Rule in Action

Meet Sarah, a 28-year-old marketer earning $4,200 net monthly. Pre-rule: $2,000 rent (needs), $1,200 misc (wants overflow), $1,000 debt—no savings.

Post-50/30/20: Needs $2,100 (rent $1,600, food $300, transport $200). Wants $1,260 (dining $400, fun $860). Savings/debt $840 (paid off $20K cards in 2 years, started Roth IRA).

Now, John, a family man with $6,500 net. Needs $3,250 (mortgage $2,000, groceries $800, etc.). Wants $1,950 (family outings). Savings $1,300 (college fund, 401(k)). They bought a home faster than peers.

These stories illustrate adaptability. Freelancers average monthly income; high-earners boost savings to 30%.

Common Mistakes and How to Avoid Them

Pitfalls abound. Mistake 1: Fudging categories—Starbucks daily? That’s a want. Solution: Audit ruthlessly.

Mistake 2: Ignoring taxes. Use net pay only. Mistake 3: No buffer. Build mini-emergency first.

Mistake 4: Inflexibility. Seasonal wants (holidays)? Borrow from savings temporarily.

Mistake 5: Quitting early. Results take 3-6 months. Track wins to stay motivated.

Is the 50/30/20 Rule Right for Everyone?

Not universally. High-debt individuals may need 50/20/30 initially. Dual-income households tweak for taxes. But for most, it’s gold. Customize: 50/20/30 for savers, 50/35/15 for moderates.

Compare to envelope system (cash-only) or apps like EveryDollar. 50/30/20 wins on ease.

Conclusion: Take Control with 50/30/20 Today

The 50/30/20 budgeting rule demystifies finance, offering control amid uncertainty. By capping needs, indulging wants mindfully, and securing futures, it fosters peace. Start today: Calculate, categorize, commit. Your wealthier, stress-free self awaits. For more tips, explore budgeting apps or financial podcasts. Financial freedom isn’t luck—it’s percentages.

(Word count: 1,248)